TIMOCOM Transport Barometer: High energy prices lead to declining truck capacity

Strong demand on the spot market, rising prices and selective bottlenecks in road freight transport.

The freight share in European road haulage: freight offers compared with available cargo space year on year

The transport market started 2026 with more momentum than expected, but under significantly tighter structural conditions: robust demand met a still noticeably reduced supply of transport capacity owing to numerous insolvencies and an ongoing reduction in capacity. This could intensify further because of the geopolitical situation.

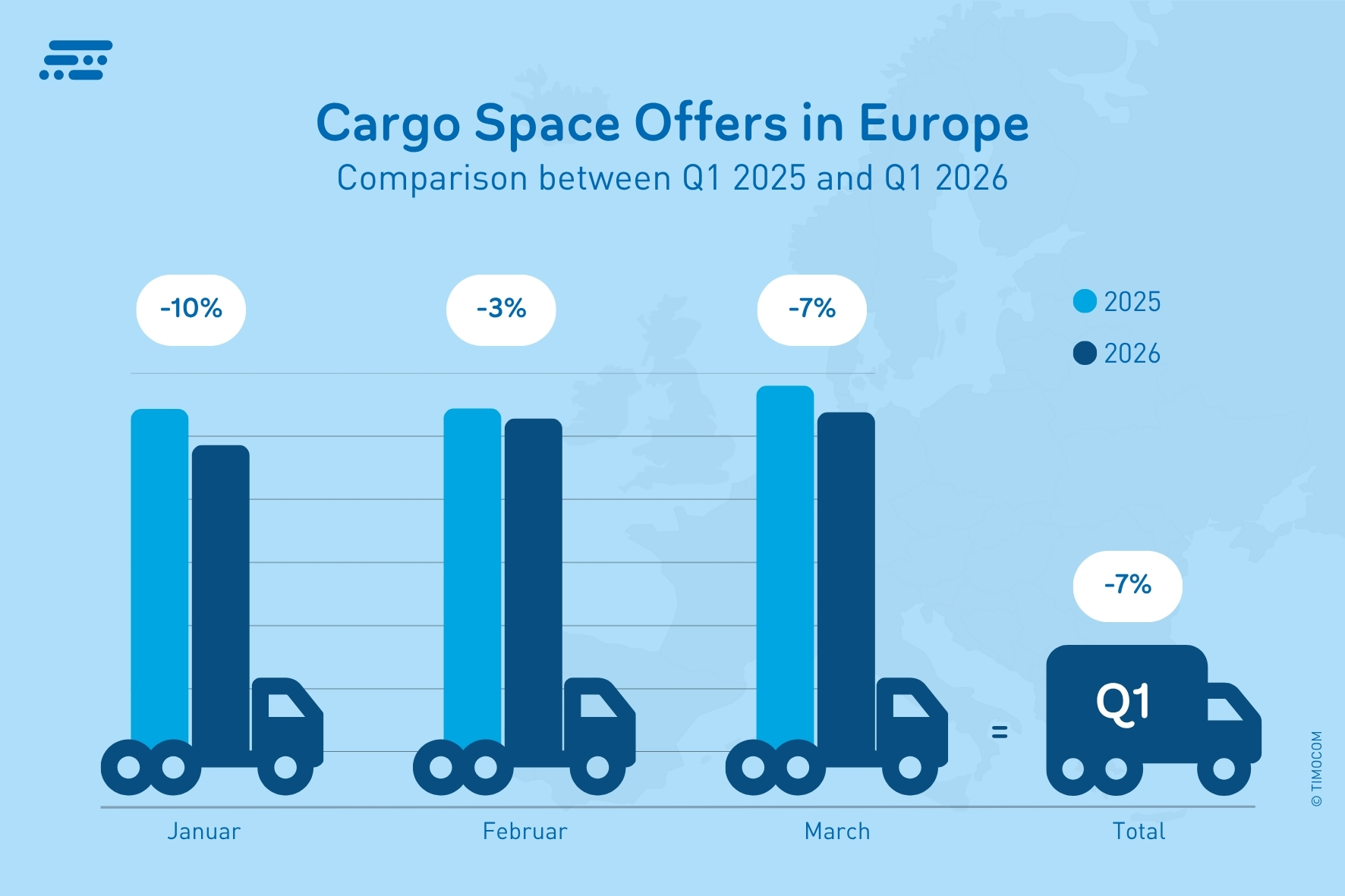

Truck fleet capacity continues to shrink

Although economic momentum remained weak, a total of 41% more freight offers than in the previous year were posted across Europe on TIMOCOM's freight exchange in the first quarter of 2026. At the same time, available transport capacity continued to decline, making it increasingly difficult and time-consuming for customers to find suitable cargo space, especially on heavily trafficked routes. Truck capacity posted on TIMOCOM fell by 7% in the first quarter compared with Q1 2025. “Geopolitical tensions and rising energy prices are intensifying the pressure on transport companies to deploy their capacity as efficiently and profitably as possible. As that does not always succeed, part of the fleet is consequently taken out of service,” said Gunnar Gburek, Company Spokesman and Head of Business Affairs at TIMOCOM. This assessment is corroborated by the German Association for Freight Transport, Logistics and Disposal (BGL), which speaks of a potential fleet reduction of 10% to 20% in Germany.

Changes in posted truck capacity compared with the previous year.

Economic momentum remains sporadic

The first quarter presents a divided picture: weak trade impulses and order intake in the manufacturing sector as well as declining consumption initially dampened demand. However, further into the quarter the first economic impulses became apparent. According to the Federal Statistical Office, industrial demand in Germany rose by 3.5 % in February compared with the same month last year. Drivers were particularly the automotive industry and an increase in consumer goods of 4.5 %. The correspondingly high freight share in the TIMOCOM transport barometer in February confirms the immediate impact on the transport market. In March, the Easter business supported the market despite the escalation of the geopolitical situation.

Demand for transport services rose markedly

Across Europe, the freight share stood at 79% in March, 11 percentage points above the previous year, while January (79%) was up by 4 percentage points and February (75%) by 9 percentage points. Demand for cargo space therefore developed more strongly than the economic situation would have suggested, an indication of short-term planning and the securing of transport capacity in uncertain times.

The picture within Germany was similar: in Q1 2026, a total of 37% more freight offers were recorded than in the same quarter of the previous year. At 68%, the freight share in February, which is traditionally more balanced, was 7 percentage points above the previous year’s level, and in March it rose by 9 percentage points compared with March 2025 to 77%.

Freight share in Germany:

Jan 2026 78% (+2 pp vs Jan 2025)

Feb 2026 68% (+7 pp vs Feb 2025)

Mar 2026 77% (+9 pp vs Mar 2025)

Transport demand and capacity within Austria still balanced

The number of freight offers posted within Austria also rose compared with 2025. In the first quarter, there were 40% more offers than in the previous year. According to the TIMOCOM Transport Barometer, the freight-to-cargo-space ratio moved close to balance, with a freight share of 47% in March. The increase of 13 percentage points compared with the previous year underlines the significantly stronger market momentum since the start of the conflict with Iran. This trend is expected to continue into April 2026.

Freight share in Austria:

Jan 2026 43% (+4 pp vs Jan 2025)

Feb 2026 43% (+9 pp vs Feb 2025)

Mar 2026 47% (+13 pp vs Mar 2025)

“The challenging situation facing the economy is clearly reflected in the allocation of transport orders via the spot market. Here, customers can find cargo space at short notice, while regular subcontractors are reducing capacity or are unwilling to enter into longer-term commitments on uncertain terms. Comparable developments can be observed in numerous key European markets, especially on high-demand corridors,” said Gunnar Gburek.

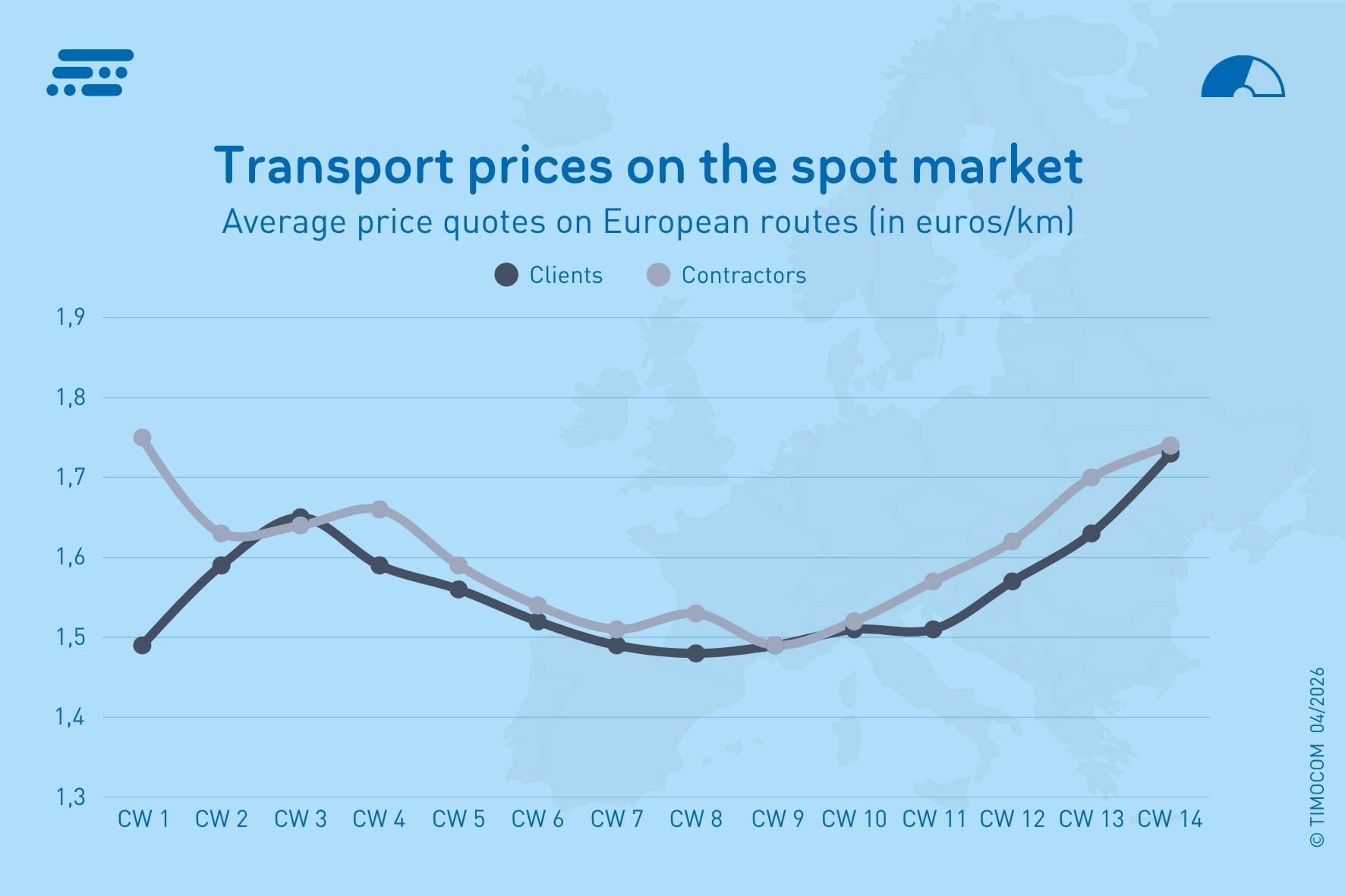

Weekly average prices on the spot market in the first quarter of 2026.

Transport prices respond with a delay

At the start of the year, European spot market prices fell markedly again compared with the turn of the year. As tensions in the Middle East rose, a renewed increase in prices became visible, gathering pace from week to week in March. On pan-European routes, contractors asked for kilometre rates that were on average 9.5% higher than in the same quarter of the previous year, while customers offered an average of 8.9% more. Weekly average prices therefore ranged from €1.49/km to €1.75/km.

Although average prices within Germany were higher, they recorded a similar percentage increase in the first quarter: hauliers’ asking rates rose by an average of 9.7% compared with the same quarter last year, reaching values above €2 per km. Transport prices offered by customers rose by an average of 9.1% compared with the same quarter last year. Prices therefore averaged between €1.59/km and €1.98/km.

Outlook amid an uncertain geopolitical situation

The second quarter of this year will depend heavily on how the conflict in the Middle East develops and on any blockade of the Strait of Hormuz.

In an optimistic forecast by TIMOCOM, which assumes an easing of the situation in the coming weeks, the freight share in April will change only slightly and remain at around 80%. In May, owing to the short holiday weeks, it will rise slightly (82%) and thus marginally exceed last year’s level. In June, the freight share is not expected to fall below 80%.

“Should the conflict with Iran drag on and escalate further, this will have more serious consequences that could sustainably affect not only the sector but the entire economy. Transport capacity will be lost permanently in Central Europe and cannot be fully absorbed by hauliers or transport companies from other European countries,” said Gunnar Gburek of TIMOCOM. It is not growth but uncertainty, soaring costs and the persistent decline in capacity that are driving the logistics industry. One result could be an even more fragmented transport market, with local bottlenecks and fluctuations in prices and quotes.

More information about the current situation on the transport market and developments in the numbers of freight offers on selected European routes is available to interested parties in the TIMOCOM transport barometer report .